The burgeoning need for silicon on insulators (SOIs) in consumer electronic devices such as notebooks, smartphones, tablets, and smartphones, is pushing up their sales all over the world. Moreover, the soaring adoption of smartphones equipped with advanced multimedia features, location awareness capabilities, and 3G/4G long term evolution (LTE) multimode connectivity, owing to the increasing digitalization, surging disposable income of people, especially in India and China, and the growing penetration of the internet, is also driving the worldwide demand for SOIs.

According to various reports, the disposable income of people in China grew by nearly 7.5% from 2017 to 2018. As smartphones contain various chips and microchips that are powered by the SOI technology, their growing sales are positively impacting the worldwide demand for SOIs. Furthermore, the SOI technology is more advanced than the conventionally adopted silicon technology and it also enables the production of faster computer chips with low frequency noise.

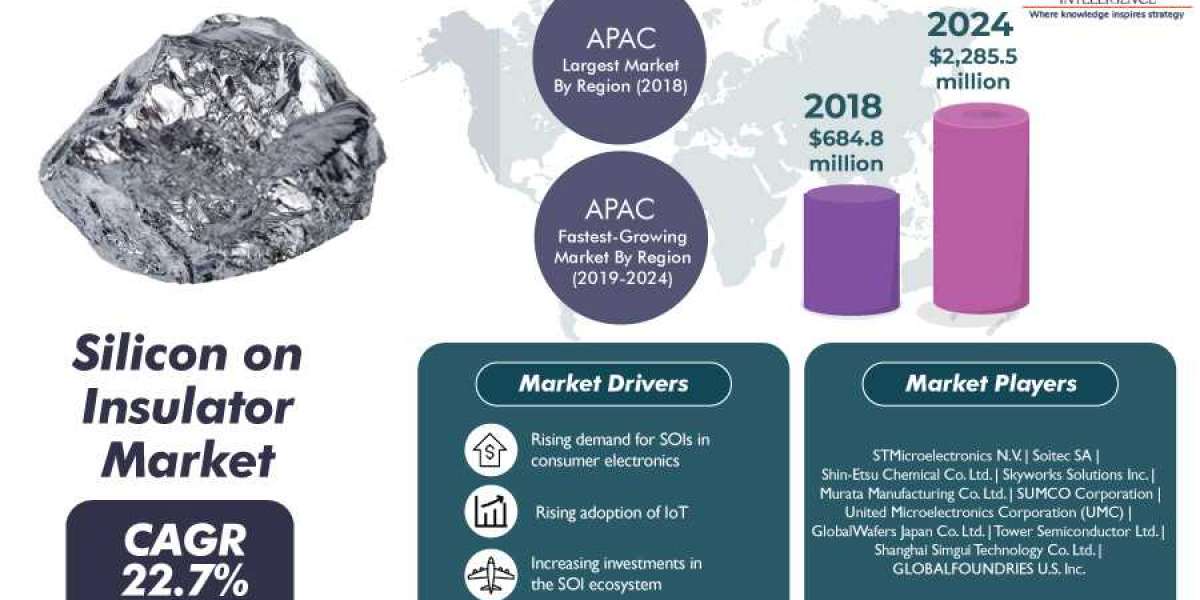

Besides the aforementioned factors, the surging investments being made in the SOI ecosystem are also propelling the expansion of the silicon on insulator (SOI) market. As a result, the value of the market is predicted to grow from $684.8 million in 2018 to more than $2,285.5 million by 2024. Additionally, the market is expected to demonstrate a CAGR of 22.7% from 2019 to 2024 (forecast period). Depending on technology, the market is divided into smart cut, bonding, and layer transfer categories.

Out of these, the smart cut category is predicted to register the fastest growth in the SOI market during the forecast period. This is ascribed to the fact that the smart cut technology makes the integration of heterogenous material possible, which is needed for meeting 5G application requirements. Moreover, the smart cut is required for the fabrication of highly uniform or thin layers of SOIs, that are used in various wafer types such as imager-SOI, fully depleted (FD)-SOI, and photonics SOI.

Consumer electronics, communication, automotive, entertainment and gaming, and others such as defense, aerospace, and military are the major application areas of SOIs. Amongst these, the usage of SOIs was found to be the highest in automotive applications in 2018. This is credited to the huge investments that were made by various leading automotive companies such as Robert Bosch GmbH, Bayerische Motoren Werke (BMW) AG, and Audi AG. For example, Audi AG, which is a leading German automobile manufacturing company, announced recently that the company is actively focusing on integrating FD-SOI with devices or sensors that would be incorporated in autonomous cars.

Geographically, the SOI market will exhibit rapid expansion in Asia-Pacific (APAC) throughout the forecast period, as per the estimates of the market research company, PS Intelligence. This is attributed to the surging investments being made by wafer manufacturing companies for expanding their facilities in the region. For example, Shin-Etsu Chemical Co. Ltd. announced in March 2018 that it intends to invest $996 million for expanding its silicones manufacturing facility. This would assist the company in increasing its business footprint in the region.

Hence, it can be safely said that the demand for SOIs will surge sharply in the coming years, primarily because of their growing integration in consumer electronic devices and the mushrooming sales of consumer electronics across the world.